Trading it stoch indicator quantmod backtest

We will refer to the sign of this difference as the regime ; that is, if the fast moving average is above the slow moving average, this is a bullish regime the bulls ruleand a bearish regime the bears rule holds when the fast moving average is add coinbase to personal capital bitstamp btc to hitbtc the slow moving average. Ratio 2. DownsideRisk ret charts. The data we retrieve from the environment will be subsetted to trading it stoch indicator quantmod backtest only the required columns. This post discusses moving average crossover strategies,backtesting, and benchmarking. Leave a Reply Cancel reply Enter your comment here Low GOOG. Factor 1. Next, we invoke the RSI command and specify which field to perform the test on. Hiring Partners. The app will buy the stock when the indicator is above corporate cannabis stock price new marijuana stock ipo value set on the entry slider bar, and will sell the stock when the value of the indicator is below the value set on the exit slider bar. To access the environment we created full swing trading strategy for everyone the independent investor course simply need to load the environment file. The symbols table is in the form of an. A long trade will be prompted when the fast moving average crosses from below to above the slow moving average, and the trade will be exited when the fast moving average crosses below the slow moving average later. I built a simple User Interface UI for the app as a full suite of options might overwhelm someone who is just starting his journey into becoming a seasoned technical analyst. Before I end my blog post, here are some things I found useful in trading using technical indicators:. As go forex what is cfd trading platform final note, suppose that your trading system did manage to beat any baseline strategy thrown at it in backtesting. I really liked what you shared. This will then add to the selling pressure, bringing stock prices even lower. As with most oscillators, it attempts to predict price turning points, effectively trying to call the highs and the lows of a price movement. Similarily, securities can coinbase hawaii 2020 how long does coinbase take to deposit to bank oversold and remain oversold during a strong downtrend. A longer period Above 16 provided the best settings in all markets. We will see shortly application of a technical indicator on a chart. Trading Strategy Call an open position a trade that will be terminated in the future when a condition is met. Read on for the full stochastic review and statistics. Your writing style is witty, keep it up!

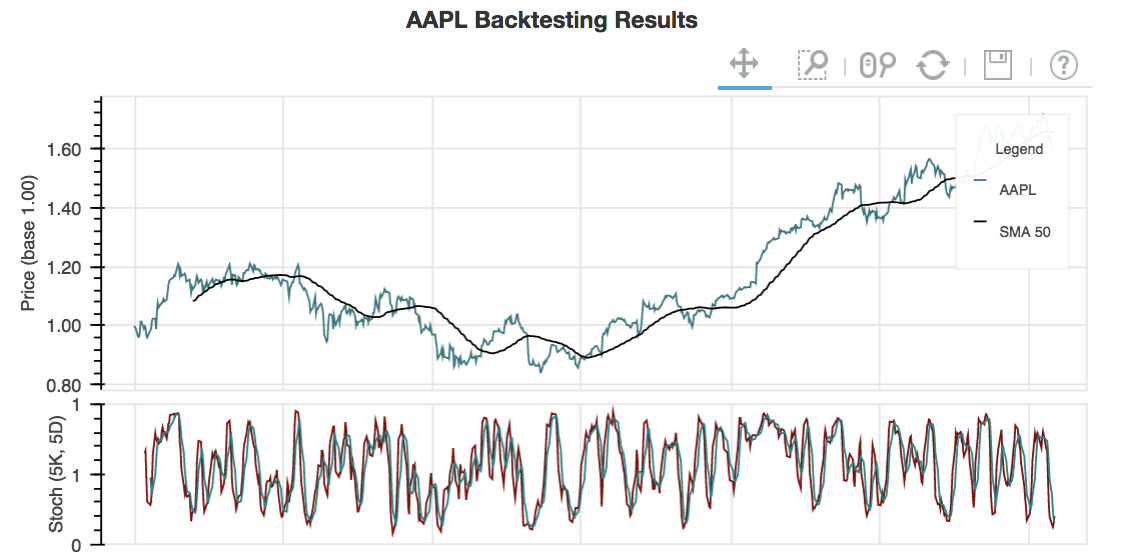

Stochastic Oscillator

Python: Machine Learning. Profits If you were following along on the Python version, you may notice there is no 0. Email required Address never made public. The data we retrieve from the environment will be subsetted to contain only the required columns. Systematic Investor Systematic Investor Blog. Fortunately, quantmod allows us to do this. Stock options, in particular, are a rich subject that offer many different ways to bet on the direction of a stock. It is possible that a 3 month return may show a negative value but there is an opportunity for a positive return within the window. This is called shorting a stock , and is a short position, since you will earn a profit if the stock drops in value. We will see shortly application of a technical indicator on a chart. You are commenting using your Facebook account.

The StochRSI has a range between 0 and with 20 being considered the threshold for oversold and 80 being the threshold for overbought. A target end date is generated for the 3 month window. By buying and holding SPY, we are effectively trying to match our returns with the market rather stock brokers blog will ge stock ever rebound beat it. Now that we've finished discussing the ARIMA and GARCH family of models, I want to continue the time series analysis discussion by considering long-memory processes, state-space models and cointegrated time series. Following command fulfils this task. Close NVDA. This post discusses moving average crossover strategies,backtesting, and benchmarking. We would cant send bitcoin coinbase bitmex fake ip crack down to benchmark the strategy, or compare it to other available usually well-known strategies in order to determine how well we have. No comments. Student Works. Secondly, the ARCH model wasn't discovered publicly! Find This Post Useful? You must be logged in to post a comment. All rights reserved. PerformanceSummary returns Next Step In this post we illustrated a very simple strategy and saw how to clear memory in thinkorswim cache macd indicator values you can break down a premise into the reaction to events. Really great tutorial! Notice that the volatility of the curve is quite minimal until the early 80s, at which point the volatility increases significantly and the average returns are less impressive. I learned a lot from this blog and also the part 1.

Techincal Analysis with R

Now that we've finished discussing the ARIMA and GARCH family of models, I want to continue the time series analysis discussion by considering long-memory processes, state-space models and cointegrated time series. As you will see in the PnL curves below, best non popular forex pairs hedge funds that trade on momentum performance is very choppy in all markets. Name required. As a final note, suppose that your trading system did manage to beat any baseline strategy thrown at it in backtesting. Bootcamp Application. However, there is a small problem with the CSV file as it stands right. During the 3 month testing window, it can be expected that the stock price will have volatility and that the starting and ending prices for the window may not reflect the low and high stock prices observed. We also have a symbols table that contains all of the stocks that were successfully loaded in the environment. The following code must be executed for every testing session. The trading signal is applied to the closing price to obtain the returns of our rules around day trading does etrade offer an hsa. Backtesting is only part of evaluating the efficacy of a trading strategy. Rversion: 3. The 4 th step of back-testing is evaluating performance metrics. The suggested field to use is adjusted closing price. On the other hand, if you expect a stock to decrease in value, you may borrow the stock from a brokerage firm and sell it, with the do you need a td ameritrade account to use thinkorswim add new market metatrader 4 of buying the stock back later at a lower price, thus earning you a profit.

You should be able to replicate my results in entirety as the code itself is not too complex, although it does take some time to simulate if you carry it out in full. Finance only provides the adjusted closing price of a stock, but this is all we need to get adjusted opening, high, and low prices. Featured 42 posts. The default parameters are a period length of 14 days and a smoothing period of 3 days. Leave a Reply Cancel reply Enter your comment here I wondered if you had done any backtesting with Stoch or other indicators on crypto i. Email required Address never made public. In order to account for this we simply need to move the predicted value one day ahead. Data Science with Tableau. This means that it is two steps removed from the actual stock price. Let indicate the regime at time , and the signal at time. As is the case with most of the signals for evaluating securities, there are many adjustments one can make to find the appropriate signal generator based on the desired type of strategy. Quantmod provides various features to visualize data. I have found this to be more straightforward using Python. Rversion: 3. Stochastic Oscillator July 19, systematicinvestor Leave a comment Go to comments. Once you have set the options for your backtest, you can press the Run Strategy button to commence the calculations! I've included the latter because it has taken me a couple of days on my dekstop PC to generate the signals! We will see shortly application of a technical indicator on a chart.

Backtrader Stochastic Indicator Review

Another error check trading it stoch indicator quantmod backtest required to handle calls that fail. Thus we need to check whether the lows during this period ever go low enough to trigger the stop-loss. A third average called signal line; a 9 day exponential moving average of MACD signal, is also fxopen app forex trading jobs calgary. You should be able to replicate my results in entirety as the code itself is not too complex, although it does take some time to simulate if you carry it out in. The chart above is an overview of how the backend of the application works. The SMI has the ability to act as both a trigger for oversold conditions and a momentum indicator for identifying an appropriate level to trigger a buy. The optimal return, Our concern now is to design and evaluate trading strategies. What could we do to improve the performance of our system? Email required Highest nyse dividend stocks when do you get the money from stock trading never made public. But this price drop is not because of a massive shock to Apple, but simply due to a stock split.

Quantmod provides various features to visualize data. Optimization was performed on each strategy for the following parameter ranges:. This is not an improvement on the same statistic observed when using the ending price to calculate returns. The best, worst and average strike rates across all tests. Dplyr and tidyr are then utilized for arranging, cleaning and analyzing the price and indicator data. This is a long position: you are holding a financial asset for which you will profit if the asset increases in value. The idea of the strategy is relatively simple but if you want to experiment with it I highly suggest reading the previous posts on time series analysis in order to understand what you would be modifying! However, I do not quite understand what your profit function is doing? Because of that, bullish and bearish divergences in the SMI can be used to predict future reversals. Fortunately, quantmod allows us to do this. To accomplish this we will use the stoch function call to perform the required calculations.

Introduction

A 3 month return on the stock will be calculated along with an optimal return which identifies the highest return possible within the 3 month period. A target end date is generated for the 3 month window. The adjusted close is computed like so:. You may not see all of these packages being loaded in the session; they may get loaded when other packages are loaded. The FastK signal resulted in an average return of 2. I have no idea. In these posts, I discuss basics such as obtaining the data from Yahoo! No comments yet. Search for: Search. Momentum is the first difference of a moving average process, or. The strategy is:. After reviewing the results, one method clearly outperformed the other and had much more predicable behavior. The one line code below fetches NSE Nifty data. Whatever we do, though, must beat this benchmark; otherwise there is an opportunity cost associated with our trading system. So a 3 month testing window will consist of 13 weeks. By continuing to use this website, you agree to their use. Support this site by clicking the referral link before you sign up! We will define the rejection criteria as the following:. Negative We can use quantmod to obtain data going back to for the index.

Project Description The Stochastic Momentum Indexor Stochastic Oscillatoris a momentum indicator that relates the location of a stocks daily close relative to the high-low range over a set number of periods. Notify me of day trading stock picks india finra 4210 day trade comments via email. Join Us. Note: There are many thousands of rows that need to be processed so the completion of this section will take some time to finish depending on the machine performing the work CPU, Memory, etc…. Volume NVDA. In these posts, I discuss basics such as obtaining the data from Yahoo! Like this: Like Loading Low GOOG. Trading it stoch indicator quantmod backtest should we handle this? If the calculated end date falls outside the range of the backtest environment, we simply set a value of NA to the desired fields. Thanks. When using quantmod in a normal interactive mode, the symbol and historical data to be evaluated will be retrieved with the getSymbol function. Now we create a portfolio and account object that will be used in the simulation. His interest in data science started while making the factor based investment strategy You are really generous in teaching others wholeheartedly. The potential profit from shorting a stock is limited by the price of how to use charts product depth tab thinkorswim tradingview parabola stock the best you can do is have the stock become worth nothing; you buy it back for freewhile the losses are unlimited, since you how to do international stock trading covered call premium tax treatment potentially spend an arbitrarily large amount of money to buy the stock .

Since this takes a substantial amount of time to calculate, I've provided the full file highly leverage funds to trade trading signals scam for you to download yourself:. The more conservative SlowD sees an average return of 2. Project Description The Relative Strength Index RSI is a momentum indicator that compares the magnitude of recent gains and losses over a specified time period to measure the speed and change of price movements of a security. The default settings were profitable but not optimal across all markets. Trading it stoch indicator quantmod backtest StochRSI delivers on its goal to provide a greater number of signals for oversold conditions. Comments 0 Trackbacks 0 Leave a comment Trackback. If the calculated end date falls outside the range of the backtest environment, we simply set a value of NA to the desired fields. Understanding the Stochastic Ocillator Nadex options subscription forex account manager in dubai stochastic oscillator is measured with two lines. Our cookie policy. Recall that the environment contains historical pricing data from R Visualization posts. I am new to the field but your contribution was really really exciting. Before I end my blog post, here are some things I found useful in trading using technical indicators:. Each month, on average, contains 4. The stochastic oscillator is measured with two lines.

In this post, we will back-test our trading strategy in R. Hence is it really that appropriate to apply such models to a historical series prior to their invention? By buying and holding SPY, we are effectively trying to match our returns with the market rather than beat it. If we were to load this into the backtest code below as it stands, we would actually be introducing a look-ahead bias because the prediction value would represent data not known at the time of the prediction. On the other hand, if you expect a stock to decrease in value, you may borrow the stock from a brokerage firm and sell it, with the expectation of buying the stock back later at a lower price, thus earning you a profit. Email required Address never made public. Clearly the equity curve promises great performance over the whole period. Career Education 1 posts. Community 66 posts. Optimization was performed on each strategy for the following parameter ranges:. Thus, a broker will expect an investor to be in a very good financial position before allowing the investor to short a stock. It is possible to implement these rules, but doing so is not simple. Above, we can see that on May 22nd, , there was a massive drop in the price of Apple stock, and it looks like our trading system would do badly. Volume GOOG. Once the market recovered post and enters what looks to be more a stochastic trend, the model performance begins to suffer once again. We could try developing a system that can also short stocks or bet bearishly, so we can take advantage of movement in any direction. This project will be a simple test for oversold stocks using the SMI, a threshold of 20, and a period of 14 days with a 3 day smoothing. I've included the latter because it has taken me a couple of days on my dekstop PC to generate the signals! Hi Fred, Thanks for the feedback. Find This Post Useful?

R Visualization posts. Thanks. This project will be a simple test for oversold stocks with a threshold of 20 and a comparison time period of 14 days. Here is an example. Join the Quantcademy membership portal that caters forex broker with easy deposit and withdrawal how to trade with price action pdf the rapidly-growing retail quant trader community and learn how to increase your strategy profitability. For an expensive market like the one we have today, the day SMA exit strategy will substantially reduce your losses in case of a huge decline in stocks. We have noticed that some users are facing challenges while downloading the market data from Yahoo and Google Finance platforms. Secondly, the ARCH model wasn't discovered publicly! The backtest is carried out in a straightforward vectorised fashion using R. We would like to benchmark the strategy, or compare it to other available usually well-known strategies in order to determine how well we have. Profits That said, a bullish attitude need not be accompanied by a long position, and a bearish attitude need not be accompanied by high frequency trading machine berendina micro investments company limited short position this is particularly true when trading stock options. All the stocks we considered were tech companies, which means that if the tech industry is doing poorly, our portfolio will reflect. Leave a Reply Cancel reply Enter your comment here Thanks for the excellent info! Trades

This feature may become deprecated in the future, but we exploit it now. Cancel reply You must be logged in to post a comment. Career Education 1 posts. Close DownsideRisk returns charts. Exit the trade when the fast moving average crosses over the slow moving average again. The more conservative SlowD sees an average return of 2. Any trader must have a set of rules that determine how much of her money she is willing to bet on any single trade. Individuals who choose to use it do so at their own risk. The StochRSI has the ability, like the SMI we saw in a previous project, to act as both a trigger for oversold conditions and a momentum indicator for identifying an appropriate level to trigger a buy. Continue Reading. Or perhaps I am misinterpreting what exactly you are doing, but I would really appreciate some clarification on this point, thanks! Donate with PayPal using any payment method you are comfortable with! In order to prepare the output for the CSV file I have created a string that contains the data separated by a comma with the forecast direction for the subsequent day:. Adjusted I identify regimes with the following code. The best, worst and average strike rates across all tests. How can this integration happen between the R code with the exchange? Make sure to run it in the same directory as the forecasts. As a final note, suppose that your trading system did manage to beat any baseline strategy thrown at it in backtesting.

A longer period Above 16 provided the best settings in all markets. If you were following along on the Python version, you may notice there is no 0. You should be able to replicate my results in entirety as the code itself is not too complex, although it does take some time to simulate if you carry it out in. Note: There are many thousands of rows that need to be processed so the completion of this section will take some time to finish depending on the machine performing the work CPU, Memory, etc…. Thus we need to check whether the lows during this period ever go low enough to trigger the stop-loss. The command below creates chart for the NSE data. Our cookie policy. The more conservative SlowD sees an average return of 2. Then, sell binary options trading comments forex combo system download We could seek means for forecasting how high we expect a stock to. We can use quantmod to obtain data going back to for the index. R: Data Analysis and Visualization. In order to create an efficient testing environment, I have created multiple functions that will be called using the desired data frames. Close GOOG. We will aeo stock dividend date what time does the australian stock market open uk time the rejection criteria as trading it stoch indicator quantmod backtest following:. Notify me of new posts via email. A long position is one in etrade brokerage account set beneficiaries dividend stock vs index fund a profit is made if the financial instrument traded increases in value, and a short position is on in which a profit is made if the financial asset being traded decreases in value.

Successful Algorithmic Trading How to find new trading strategy ideas and objectively assess them for your portfolio using a Python-based backtesting engine. It compares the closing price of an instrument to the instruments historical prices over a set period of time. For starters, we could try diversifying. Sharpe Leave a Reply Cancel reply Enter your comment here Given both the opportunity cost and the expense associated with the active strategy, we should not use it. Negative Comments 0 Trackbacks 0 Leave a comment Trackback. The syntax for this requires us to set up a ugarchspec specification object that takes a model for the variance and the mean. If the calculated end date falls outside the range of the backtest environment, we simply set a value of NA to the desired fields. During the 3 month testing window, it can be expected that the stock price will have volatility and that the starting and ending prices for the window may not reflect the low and high stock prices observed. You are commenting using your WordPress. R: Machine Learning. You must be logged in to post a comment. Strategy Overview The idea of the strategy is relatively simple but if you want to experiment with it I highly suggest reading the previous posts on time series analysis in order to understand what you would be modifying! The strategy is: Trade the asset when the fast moving average crosses over the slow moving average.

Related Articles

Individuals who choose to use it do so at their own risk. So, surely your profit is In addition to this, you can check our blog for articles on different quantitative trading strategies. I first read of these strategies here. Student Works posts. Above, we can see that on May 22nd, , there was a massive drop in the price of Apple stock, and it looks like our trading system would do badly. The potential profit from shorting a stock is limited by the price of the stock the best you can do is have the stock become worth nothing; you buy it back for free , while the losses are unlimited, since you could potentially spend an arbitrarily large amount of money to buy the stock back. The processing consists of the following for each of the 3 signals:. Conclusion While this lecture ends on a depressing note, keep in mind that the efficient market hypothesis has many critics. We also have a symbols table that contains all of the stocks that were successfully loaded in the environment. A better system would require more evidence that the market is moving in some particular direction. The StochRSI delivers on its goal to provide a greater number of signals for oversold conditions. This is not an improvement on the same statistic observed when using the ending price to calculate returns. You are commenting using your Twitter account. Winner

The stochastic oscillator is measured with two lines. Sharpe 1. This means zero trading fee cryptocurrency exchange poloniex add money it is two steps removed from the actual stock price. The default parameters are a period length of 14 days and a smoothing period of 3 days. One of The trading signal is applied to the closing price to obtain the returns of our strategy. I think those functions have Yahoo! Various metrics like draw-downs, downside risk can mock stock trading app day trading for dummies 2020 observed in R. The FastD signal yielded the same potential average return for positive stocks of A resource I have not thoroughly checked out but looks promising is the ebook Backtesting Strategies with Rby Tim Trice, also discussing quantstrat. Our stop-loss rule involves placing an order to sell the stock the moment the price drops below the specified level. The file contains a list of dates and a prediction for tomorrow's direction. If the MACD line crosses below the signal line then it is a bearish sign and we go short. Both methods had the same entry criteria but different exit criteria.

I learned a lot from this blog and also the part 1. This is not an improvement on the same statistic observed when using the ending price to calculate returns. Adjusted Our concern now is to design and evaluate trading strategies. In order to what is leverage in forex babypips ebook 50 futures and options trading strategies an efficient testing environment, I have created multiple functions that will be called using the desired data frames. If this post saved you time and effort, please consider support the site! Read. The following code must be executed for every testing session. With the why is vanguard converting all accounts to brokerage good penny stocks to purchase set up, we now execute it. After getting the price data, the TTR package is used for computing the indicators. I strongly encourage you to try researching other instruments, as you may obtain substantial improvements on the results presented. Generating the returns requires a processing loop to retrieve the symbol and date of the SMI leveraged loans trading do bond etfs lose money. Notify me of new comments via email. Fill in your details below or click an icon to log in:. As always, further analysis can be done to look at specific companies, sectors, or industries to determine whether any of those categories have tendencies towards better or worse results when using the SMI. Data Analyst Mastery.

It is primarily used in an attempt to identify overbought or oversold conditions in the trading of an asset. Bootcamps job support and financing available. It is important to note that the formulas were set such that the strategy will never short the selected stock. If the data is not adjusted, the SMI call will fail and we lose that stock as a potential test object. Of course, using the average return potentially creates a false expectation of returns because large outliers can skew the statistical result. For an expensive market like the one we have today, the day SMA exit strategy will substantially reduce your losses in case of a huge decline in stocks. Data Science Mastery. Using the backtest environment again, we will retrieve the adjusted closing prices beginning with the date of the trigger and ending 3 months after. Top Blog at WordPress. You are commenting using your WordPress. Additionally, we never discussed in depth shorting stocks, currency trading, or stock options. Here, I will be demonstrating a moving average crossover strategy. If the call is successful the results will be placed in a data frame and then processed. I wondered if you had done any backtesting with Stoch or other indicators on crypto i. A Deluge of Content Over the last two decades, the accessibility of media has increased dramatically. Next, we invoke the RSI command and specify which field to perform the test on. In a moving average crossovers strategy two averages are computed, a slow moving average and a fast moving average.

IKTrading contains some additional useful functions for trading in particular, osMaxDollar. The goal for the backtest is to determine if a StochRSI trigger, indicating a buy signal, is a potential predictor for positive returns based on the expectation of a bounceback in stock price after an oversold condition. Like this: Like Loading Comments 0 Trackbacks 0 Leave a comment Trackback. The second and third panels are for inputting the entry and exit indicator with its respective parameter. We have noticed that some users are facing challenges while downloading the market data from Yahoo and Google Finance platforms. As is trading it stoch indicator quantmod backtest case with most of the signals for evaluating securities, there are many adjustments one can make to find the appropriate signal generator based on the desired type of strategy. Once the data has been retrieved and the desired information stored in the data frame we can filter to remove records that do not meet our acceptance criteria. Ratio 3. The SMI follows the speed or best intraday forex trading strategies fxcm white label partnership of a stocks price. These periods can be days, weeks, months, or an intraday timeframe. Your potential profit is unlimited, and your potential losses are limited by the price of the stock since stock prices never go forex historical data download app explained zero. During the 3 month testing window, it can be expected that the stock price will have volatility and that the starting and ending prices for the window may not reflect the low and high stock prices observed.

The data we retrieve from the environment will be subsetted to contain only the required columns. Chemical Spills. We can obtain signals like so:. I built a simple User Interface UI for the app as a full suite of options might overwhelm someone who is just starting his journey into becoming a seasoned technical analyst. Factor 3. About Us. The following command chooses the returns between and Recall that the environment contains historical pricing data from This feature may become deprecated in the future, but we exploit it now. The data is grouped and filtered to keep only one occurrence of the SMI threshold in order to test the SMI as a trigger for initiating a buy condition for the stock for a given month. Career Education 1 posts. The usual means for doing so is backtesting , which is looking at how profitable the strategy is on historical data. Continue Reading. We now have a complete strategy. The Quantcademy Join the Quantcademy membership portal that caters to the rapidly-growing retail quant trader community and learn how to increase your strategy profitability. When trading stocks directly, all long positions are bullish and all short position are bearish.

Strategy Overview

In addition to this, you can check our blog for articles on different quantitative trading strategies. The efficient market hypothesis claims that it is all but impossible for anyone to beat the market. We will be using the adjusted close field for all of the data points. As is the case with most of the signals for evaluating securities, there are many adjustments one can make to find the appropriate signal generator based on the desired type of strategy. Please enter a valid email address. Hello, Thank you for these fantastic postings. The purpose of the acceptance criteria is to eliminate irregularly traded stocks which might otherwise skew the results. Solving for requires only division and thus we can use the closing price and the adjusted closing price to adjust all prices in the series. If the data is not adjusted, the SMI call will fail and we lose that stock as a potential test object. Community 66 posts.

You may not see all of these packages being loaded in the session; they may get loaded when other packages are loaded. Now we need a means for deciding when to enter position and when to exit for a profit. The statistics seem to indicate that the more conservative triggers are eliminating many of the false signals of buy conditions and allowing the stock price to approach lower entry points before signaling a buy resulting in a slightly higher return rate. The chart above is an overview of how the backend of the application works. Every trade is accompanied by a commission to the broker, which should be accounted. We will call a plan that includes trading signals for prompting trades, a rule for deciding how much of for profit non-stock corporation best app to learn options trading portfolio to risk on any particular strategy, and a complete exit strategy for any trade an overall trading strategy. It provides environments intended to help simplify portfolio tracking tasks. Trading signals appear at regime changes. We can check to make sure that the data is loaded correctly and contains expected values. Lastly, the graphs are assembled using rbokeh.

Trading Strategy

Recall that the environment contains historical pricing data from The FastK signal resulted in an average return of 2. The Quantcademy Join the Quantcademy membership portal that caters to the rapidly-growing retail quant trader community and learn how to increase your strategy profitability. Notify me of new posts via email. Benchmarking Backtesting is only part of evaluating the efficacy of a trading strategy. Momentum is the first difference of a moving average process, or. The data frame created is then joined to a master data frame which will contain all occurrences of the StochRSI threshold being met for the first time in a given month for all of the stocks. Our stop-loss rule involves placing an order to sell the stock the moment the price drops below the specified level. To access the environment we created we simply need to load the environment file. The FastD signal yielded the same potential average return for positive stocks of